Last year in September, Barclays carried out the very first transaction using blockchain technology. A process that usually takes 6 to 7 days to be completed is conducted in less than 4 hours. Approximately 80% of the banks are now working to develop their own blockchain technology because of the wonders being done by it.

Other big names like IBM and NASDAQ are also in action to come up with solutions for easier and quicker transactions. The biggest value point of blockchain is that it eliminates the involvement of third parties and establishes vague trust between the two strangers. Just like blockchain is replacing middlemen, is it going to extinguish the need for human capital too in near future?

Throughout the history of the world, there are both winners and losers whenever a paradigm shift takes place. Today, the cryptocurrency market is worth a mind-boggling 100 billion dollars or even more than that. Each startup is already relying on blockchain to push trustworthiness and transparency in the digital ecosystem and to lure more investors.

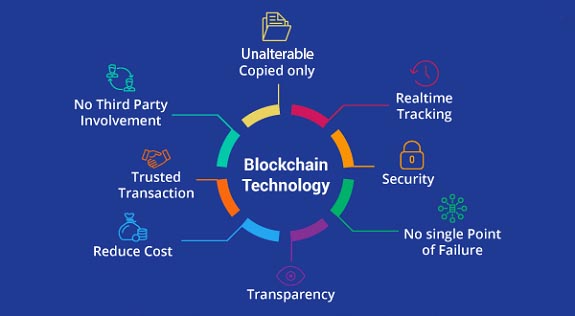

Blockchain technology enables companies working in the accounting and supply chain management etc. to carry out permanent decentralized transactions. It has the tendency to eliminate human error and to perform any given task in a limited time. There are no delays or additional costs involved and the distributed ledger allows making the authentication of various transactions easier too.

Not just finance, businesses belonging to different niches including healthcare, real estate, and even food are trying to figure out how blockchain can help them in achieving their goals faster. People are actively looking for talent in the blockchain space with the number of postings regarding such skills being trebled on LinkedIn in the past year.

With the penetration of blockchain in different industries, there are high chances of human capital compromising but are humans ready to accept this disruption? A survey conducted by the Chartered Institute of Management Accountants (CIMA) and Thomson Reuters revealed that only 4% of the accountants considered blockchain to be disruptive to their industry. They fail to realize that blockchain is imposing more threats than machine learning on humans.

Former CFO of J. P. Morgan’s Investment Bank and CEO of Digital Asset Holdings, Blythe Masters says. “You should be taking this technology as seriously as you should have been taking the development of the internet in the early 1990s.”

The ultimate dilemma of this situation is that blockchain is ready to become a ground source for all the businesses just like the internet is today. Not incorporating it means that the businesses will be lagging behind and including it will eventually decrease the need for human capital making it obsolete.

Even a startup like CannaSOS which aims to become a comprehensive advertising and social network platform for the cannabis industry is relying on this technology to discover wide horizons bitcoinx. They are able to achieve their goals and targets related to bringing flexibility to the regulations regarding the cannabis industry. Through their Pre-ICO, they are already gaining a lot of investors and people who believe in their cause. Despite the possible threats imposed by blockchain technology, it is here to stay and take the world by storm.

The flexibility for payment options has become a luxury rather than an expectation within eCommerce.…

Online shopping works the same way. If customers have to go through multiple steps just…

TinaKitten is a well-known Twitch star with over 1.9 million followers. She is recognized for…

Rachel Pizzolato Bio/Wikipedia: Rachel Pizzolato is a versatile TV host, fashion model, and TikTok star…

Did you know that the world of digital marketing is quite dynamic? In this online…

Have you ever experienced muscle spasms or excruciating pain while running, walking, or even lying…

View Comments